Forex Daytrading Strategy : An Application of the Gaussian Mixture

Model to Marginalized Currency pairs in Africa

Stratégie en Daytrading sur le Forex: Une Application du

Modèle de Mélange Gaussien aux Paires de Devises

Marginalisées en Afrique

Yvan Jorel Ngaleu Ngoyi, PhD in Scientific Algorithmic Trading, E-mail: official@refonteinfini.com

ElieNNgongang, Professor of Economics and Quantitative Techniques, Email: ngongother@yahoo.fr

Abstract: In this article, we build a Daytrading strategy by applying a

Gaussian Mixture Model (GMM) to so-called “marginalized”

African currency pairs. With a sample of data covering the period of

01/01/2010 to 05/15/2021 and downloaded in real time from the US

Federal Reserve (FRED) website and the Yahoo Finance platform, we

found that by including four explanatory variables in the Gaussian

mixture model, the GMM independently estimates the returns of the

following six African currency pairs with an average accuracy of

approximately 56.379%: USDZAR, USDNGN, USDEGP, USDMAD, USDMUR and

USDKES. The accuracy of the estimations obtained with the GMM on the

returns of the USDZAR currency pair is the highest (73.887%) among the

six currency pairs studied in this work. Based on the above results,

we have built a trading robot (based on the GMM) that runs in real

time and which we have deployed in production in the exchange rate

market. In general, by adjusting several parameters of the GMM, our

trading robot achieves overall positive daily gains.

Résumé : Dans cet article, nous construisons une stratégie en

Daytrading en appliquant un modèle de mélange gaussien

(GMM) aux paires de devises africaines

dites « marginalisées ». Avec un

échantillon de données s’étalant sur la

période 01/01/2010 à 15/05/2021 et

téléchargé en temps réel sur le site de la

Reserve Fédérale Américaine (FRED) et la

plateforme Yahoo Finance, nous avons constaté qu’en

incluant quatre variables explicatives dans le modèle de

mélange gaussien, le GMM estime indépendamment les

rendements des six paires de devises africaines suivantes avec une

précision moyenne d’environ 56,379% : USDZAR,

USDNGN, USDEGP, USDMAD, USDMUR et USDKES. La précision des

estimations obtenues avec le GMM sur les rendements de la paire de

devise USDZAR est la plus élevée (73,887%) parmi les six

paires de devises étudiées dans ce travail. Fort des

résultats ci-dessus, nous avons construit un robot de trading

(à partir du GMM) qui tourne en temps réel et que nous

avons déployé en production sur le marché des

taux de changes. De manière générale, en ajustant

plusieurs paramètres du GMM, notre robot de trading obtient des

gains journaliers globalement positifs.

Keywords: Strategy, Daytrading, GMM, so-called “marginalized”

currency pairs, trading robot.

Mots clés : Stratégie, Daytrading, GMM, paires de devises dites

« marginalisées », robot de

trading.

Introduction

New financial assets have appeared in the last ten years on the

currency market (Forex). These new assets generally concern the parity

between major currencies[1] and popular cryptocurrencies.[2] Cryptocurrencies today have an insignificant influence on the

currency market. Indeed, the volume of transactions on

cryptocurrencies is much lower than that on Forex (reminder: the daily

trading volume on Forex is about 6600 billion US dollars) . It is very

important to study the new joint ecosystem in which exchange rates and

cryptocurrencies are bathed. A good anticipation of the future of

exchange rates and digital currencies can lead to investment

opportunities and may also prevent drifts (crises, bubbles) that may

arise from these new currencies.

The objective of this article is to construct a daily strategy, based

on the Gaussian Mixture Model (GMM), serving as an algorithmic trading

tool for participants in the currency market. In other words, our

objective in this article is to build a trading robot that runs in

real time around the clock from the GMM and anticipates the evolution

of returns on African currency pairs. Several financial firms are

interested in trading robots and/or the empirical validation of models

that they can use as a basis to develop a trading algorithm that they

will then connect to the market to increase their returns. We can

cite, for example, the companies Quantiacs and QuantConnect, which

receive the models developed and programmed by any researcher, connect

them to the market, and share the profits with the researcher if the

model is profitable.

The stationarity hypothesis is regularly violated when applied to

financial product data. The violation of this assumption in financial

markets renders almost all autoregressive models (including ARCH and

GARCH family models) ineffective in anticipating and/or predicting

stock price movements (Wang et al, 2019).

Long forgotten by scientists, parametric models have flourished over

the last twenty years thanks to the exponential growth in the

computing power of machine processors, the increase in the size of

machine memory, the increase in machine disk space and the

democratization (lower prices) of machines (servers, laptops,

mobile phones, ...). This phenomenon is empirically observable

by Gordon Moore's first and second laws (1965). This observation

also shows us that most parametric models that have many parameters

and require good computing power (unless we want to run a

simulation/calculation and wait a few days to get the outputs) can now

be computer by everyone from the moment we have a laptop or a mobile

phone. Thus, in this article, we propose to use the Gaussian Mixture

Model (GMM (1894)) and the Hidden Markov Model (HMM), both

accompanied by the Johnson Su model (1949), to build a Forex trading

robot capable of opening one or more positions in a day, take

profits, and close those positions on the same day. In other words, it

is about building a Daytrading strategy on Forex by applying the

Gaussian mix model to African currency pairs. s

The contribution of this article is a first: unless we are mistaken,

and after having gone through the financial literature, we think that

it is a first time in the financial literature that a robot built from

the GMM-HMM[3] and trade on African currency pairs (and running in real time

24 hours a day on the Forex market) has been developed, coded, and

published by researchers. The estimates of the parameters of the robot

using the GMM-HMM were made from a sample of data extending over the

period 01/01/2010 to 15/05/2021 and downloaded in real time from the

website of the US Federal Reserve (FRED) and the Yahoo Finance

platform. The remainder of the article is organized as follows:

section (1) presents the literature review; section (2) discusses

research questions and hypotheses; section (3) describes the

methodological approach; section (4) presents and discusses the

results.

1. Financial Markets Literature Review

Financial markets are the markets in which short-, medium- and

long-term demand and supply of capital meet. They are also markets in

which individuals, private companies and public institutions intervene

to trade, buy and/or sell financial securities.

In this section 1, we present on the one hand the context and the

review of the literature, i.e. the microstructure of the foreign

exchange market, the different participants in the Forex market and

the different types of algorithmic trading; On the other hand,

we present a review of the literature on models commonly used in

financial markets, i.e. we review the scientific literature on

linear models and nonlinear or probabilistic models generally used in

finance.

1.1 Background and literature review

Financial markets are markets in which individuals, private

companies and public institutions can trade securities, commodities

and other assets at prices that reflect supply and demand[4].

The foreign exchange market is the market in which all participants

who want to sell or buy one currency in exchange for another currency

meet. Transactions on the foreign exchange market have increased by

more than a third over the last three years, reaching 6.6trillion

dollars (more than 5,400 billion euros) per day, or about 90% of

Japan's annual GDP (Bank of International Settlement, 2004 and

2019).

The presence of trends and volatility in the foreign exchange markets

between 2001 and 2004 led to an increase in commercial dynamism, where

investors took large positions in foreign currency. This then led to

an appreciation of trends and short positions by decreasing

currencies. This decline in currencies has squeezed economic

activity. To this end, most central banks have responded by increasing

liquidity in the economy. These trends have also led to an increase in

hedging activities against exchange rate fluctuations (Idvall et al,

2008).

On the Forex, there are six main players to varying degrees:

commercial banks, institutional investors, multinational enterprises,

central banks, brokers and individuals (Idvall 2008 , Guerreiro

2016).

The Forex market can be organized into two main compartments: the

interbank market and the foreign exchange market open to the rest of

the world. Interbank market transactions take place between central

banks and commercial banks (Guerreiro, 2016).

Foreign exchange markets are often called "commercial" or

"dematerialized" because of their electronic nature: they

take the form of computer networks between financial institutions.

The Nasdaq was one of the first over-the-counter markets where

technology replaced the physical interaction of humans (Hendershott,

2003).

With the boom in technological advancements in the finance industry,

algorithmic trading (TA) and high frequency trading (HFT) are welcome

and accepted for trading anywhere in the world. Within a decade, TA

and HFT will be the most common means of trading in developed markets

and will spread rapidly in developing economies.

In discretionary trading, the maximum risk comes from decisions made

under the influence of the trader’s uncontrolled emotions. In

most cases, these emotions can lead to decisions that cannot be

logically justified. Therefore, in order to make a profit, it becomes

extremely important to not only have a profitable strategy, but also

to have control over one's emotions (Kabbaj, 2011).

(Eriksson 2007; Moore 2017) Algorithmic trading means turning a

trading idea into a trading strategy via an algorithm. The trading

strategy thus created can be "backtested"[5] with historical data to check if it will give good returns on

real markets. The algorithmic trading strategy can be executed

manually or automatically. Thus, algo traders use algorithms to

make buy/sell decisions or to optimize their luck in order to make a

profit on the investments they make. The algorithms are modified

according to market conditions, type of financial instruments,

etc.

Quantitative trading involves using mathematical models and

advanced statistics for the creation and execution of trading

strategies. The mission of "quants" is the mathematical

modeling of trading strategies.

Automatic trading means that order generation, submission and order

execution process are completely automatic.

Trading strategies can be categorized into low frequency, medium

frequency, and high frequency strategies depending on how long orders

are held. High frequency strategies are algorithmic strategies that

are executed in an automated manner in the blink of an eye, usually on

a timescale of seconds. These strategies hold their positions for a

very short time and try to take advantage of very small profit spreads

per trade. These strategies also involve executing millions of trades

every day. In other words, the THF is the TA where orders are made at

the speed of light (about 1 nanosecond), for purely speculative

purposes and positions are closed before the stock market closes. THF

and TA can be considered daytrading strategies. As we will see below,

daytrading consists of taking positions on average time units and

closing your position at the end of the day (i.e. before 24

hours).

Machine Learning and Deep Learning Trading (Moore, 2017): There is

sometimes confusion between Artificial Intelligence (AI), Machine

Learning (ML) and deep learning or Deep Learning (DL). AI is a much

larger space that spans ML and DL. While ML is a part of AI, DL is a

subset of ML.

All of these applications are based on the concept of learning from

past data and predicting the outcome of a new and unseen situation

whose true value will be incorporated into the database and so on;

This is done the same way humans learn.

Behind all these trading strategies, there are statistical and

econometric models such as linear regression models, multidimensional

statistical models (principal component analysis, factorial analysis

of correspondences, etc.), autoregressive models (ARMA, ARCH, GARCH) ,

mixture models (Gaussian mixture models, binomial mixture model,

…), Markov models. The Gaussian mixture model is a particular

model because it can model any data set but with a random margin of

error (Attar, 2012). It is a model that is both additive and

multiplicative in the sense that it is a sum of Gaussian models each

modeling a cluster, each being assigned a weight (probability) which

determines the individual importance of each cluster in the set of

data. This robustness of the Gaussian Mixture Model (GMM) is one of

the reasons that motivated us to apply the GMM to Forex data.

Depending on the time units on which the Forex players trade, we can

group the strategies of these investors into three categories:

"scalping" consists of taking positions on very short time

frame units (less than 5 minutes ) and stay there for a few minutes;

“daytrading” consists of taking positions on average time

units and closing your position at the end of the day (i.e. before 24

hours) (Thukral et al, 2013); “swing trading” consists of

taking positions on long time frames (between 4 hours and 1 day) and

staying there for a few days (Thukral et al, 2013).

The microstructure of financial markets is one of the branches of

microeconomics that studies the mechanisms by which prices are formed

and influence the market. This discipline is based on the development

of mathematical models to determine prices. German (1976) is one of

the first authors to work on the microstructure of financial markets.

He considers market activity to be a stochastic process that follows a

Poisson law. Its objective is to describe the microstructure of

financial markets over time. The author then develops two models which

are still used today to determine the implications of prices on the

markets: one of the models considers that the market is purely

price-driven (absence of market-makers or market-makers) and the other

considers a market in which prices are centralized at the level of

market makers. Demsetz (1968) was the first to research the

determinants of transaction costs in financial markets. His study

applies data from the New York Stock Exchange (NYSE) because he

considers that the NYSE is the largest stock exchange in the world.

The objective of his article is to determine the explanatory variables

that influence the spread (bid/ask) and to measure the influence that

brokerage intermediaries could have on the distribution of

transactions and prices. From the time series of the share prices of

each company listed on the NYSE, Demetz (1968) constructs a

multivariate econometric process. He finds a negative and significant

relationship between the distribution of transactions and the size of

the market maker; The size of the market maker being measured

according to its own funds. It also identifies three sources of costs:

order processing costs, inventory holding costs and information

asymmetry costs.

The variation of the Spread often leads to costs called

"Slippage" which is the difference in cost between the one

at which the order would like to be executed and the one where it was

actually executed. This can be a problem when you want to get out

quickly or if you have small goals (stop loss[6] and take profit[7]). Stop loss and take profit have their origins and

justifications in the theories of behavioral finance, led by Daniel

Kahneman (1981). From laboratory experiments, Daniel Kahneman

and Amos Tversky show in 1979 how individuals asymmetrically

evaluate their expectations of loss and gain. To give a very

simplified example, the pain of losing an amount X (e.g. 1000

euros) could only be offset by the pleasure of winning kX (e.g. 2000,

or even 3000 euros).[8] This implies that when a trader is in a loss situation, he

tends to lose more and more because he hopes that the situation

will turn around and that when he wins, he tends to take his gains

quickly because he does not bear the loss. Two minimal solutions to

these psychological biases are on the one hand stop loss and take

profit and on the other hand TA and HFT. These psychological biases

amplify volatility and clustering in markets (Kabbaj, 2011).

Information (that which has a direct impact on the value of an asset

such as economic information) also plays an important role in the

behavior of market participants. John Muth (1961) was the first author

who introduced the theory of rational expectations to take into

account the influence of information in negotiations between economic

agents, especially when studying how a large number of individuals, d

companies and organizations make choices under uncertainty. But it was

Robert Lucas who would make this theory popular in the 1970s when he

used it to critique monetarist and Keynesian theories of business

cycles; This critique is generally known as the "Lucas

Critique". Lucas' idea is that economic agents can very well

exploit past and present information to make rational anticipations

and make good decisions, so that on average, they are not wrong. In

other words, agents can well anticipate the evolution of economic

quantities according to their conditional expectations and known

information. This does not mean that individuals are perfect preachers

or that they are omniscient but that they have the same information.

But, still during the 1970s, Akerlof (1970) shows on a second-hand car

market that information is not perfect on the markets because there

are insider trading, anti- selection and moral hazard. This presence

of information asymmetry in the markets has also been studied by

Joseph Stiglitz[9] in the context of market imperfections in economics. This means

that information is imperfect in the markets because there are also

costs associated with obtaining information. A well-informed investor

has an advantage over an uninformed investor because the well-informed

investor can better anticipate and, thus, he can minimize his risks

and increase his return. Investors looking for the right information

on the markets will create a mimicry effect which consists, for an

operator, in the imitation of his environment. This effect generates a

kind of crowd psychology in the market that follows the law of large

numbers because if the vast majority of investors believe that the

price of an asset will increase, then this price will increase.

Another Nobel laureate who also worked on information is

Eugène Fama (1970). His work on the determination of asset

prices earned him the Nobel Prize in 2013. He developed the concept of

"efficiency of financial markets" which dates back to the

theory of efficient markets of Louis Bachelier (1900). According to

Fama, a market is said to be efficient if the prices fully reflect the

information available on the market at all times.

According to Brealey et al (2006), the hypothesis of market

efficiency implies: we must always take into account the intrinsic

variable (or economic variable) that affects the price of a share, and

we must not be satisfied only with asset prices and price memory. The

first implication is very interesting because it will allow us to take

economic variables into account in our model. We then construct a

Gaussian mixture model (GMM) in which we introduce both the returns

(time series of returns) of the exchange rates and the fundamental

macroeconomic variables that have significant effects on the rates (we

rely on the literature theoretical and empirical to choose these

fundamental variables).

1.2 Literature review of models generally used in financial

markets

This article is part of a capitalist and purely selfish economic

current to the Adam Smith (Adam Smith: Theory of Moral Sentiments, 1759). "As

selfish as man may be supposed, there are evidently certain principles

in his nature which lead him to interest himself in the fortunes of

others, and which make their happiness necessary to him, although he

derives nothing from them. other than the pleasure of seeing them

happy" (Adam Smith: Theory of Moral Sentiments, 1759; translate

in French by Biziou, Gautier, Pradeau, PUF, Quadrige, 1999, p.

23). It is not because this article is capitalistic that it does not

contribute to the very good development of society. The individual (or

the company or the bank or the institution or the state) who will

apply the GMM model developed in this article (to his currency

portfolio on the Forex market) will generate profits which he can then

spend or invest in his country; this expenditure will have a more or

less negligible positive impact on the overall consumption of the

country, which in turn has a positive impact on growth and therefore

on the development of the country.

The formal and serious analysis of the risk/return couple was first

proposed in 1952 by Markowitz. Following the work of Markowitz, Sharpe

proposed in 1964 a complementary model to Markowitz's analysis.

The model proposed by Sharpe is known as the “Capital Asset

Pricing Model or CAPM” or, in French, “Modèle

d’Equilibre des Actifs Financiers ou MEDAF”. This

model determines the relationship between the expected return of an

investment and the return of the market portfolio or systematic risk

or risk that cannot be diversified. In 1976, Ross proposed a

multifactorial CAPM approach. This approach of Ross assumes that the

return of an asset is explained by several factors and not just a

single factor (the profitability of the market portfolio) as thought

by Sharpe (1964). This also means that the risk associated with an

investment comes from several sources and therefore the CAPM contains

several sources of systematic risk. Ross's (1976) model is known

as Arbitrage Pricing Theory or "APT".

The Markowitz model (1952) measures the expected return of an asset

and the associated risk. The CAPM or in French “MEDAF” is

in a way a linear regression of the return on the asset on a single

explanatory variable (the return on the market portfolio). The

Arbitrage Pricing Theory (APT) is a generalization of the CAPM because

in the APT, several factors explain the profitability of the assets

and each of them constitutes a source of systematic risk. These models

are unrealistic because they are based on several assumptions. For

example, the assumption on the independence of residuals is not

entirely realistic because in a market there are often correlations

between prices.

Despite these limits, the CAPM and the APT remain important for

modeling the profitability of financial assets because they can be

associated, for example, with autoregressive models (to build, for

example, ARMAX) and probabilistic models (to, for example, build

latent models of probit, logit, Markov models).

Two papers published in 1927 paved the way for autoregressive

processes and moving averages: the paper by Yule (1927) ('On the

method of investigating periodicities in disturbed series with sepcial

reference to Wolfer's sunspot numbers') and that by Slutzy (

1927) ('the summation of random causes as the source of cyclical

processes'). The prices of the different stock prices are supposed

to reflect all the market information and we can therefore treat the

time series of the prices of the different stock prices as

autoregressive processes. The fact that prices always reflect the

information available in a market was first called “financial

market efficiency” by Eugène Fama (1970). Fama traces

what he calls the "theory", or the "hypothesis",

of "efficient financial markets" to Louis Bachelier (1900).

The vague formulation he gives to this "theory" ("a

market in which prices 'fully reflect' and always the

available information is called efficient") had the consequence

that it gave rise to (at least) two very different interpretations. On

the one hand, a market would be "efficient" if the price of

securities follows a random walk, making its evolution unpredictable

(this also means that we cannot beat the financial markets); on the

other hand, a market would be "efficient" if the price of

securities corresponds to their "fundamental" or

"intrinsic" value, thus allowing an optimal allocation of

resources.

In the case where an autoregressive process  is not stationary, it can be stationarized using the primary

difference filters (Monbet, 2011).

is not stationary, it can be stationarized using the primary

difference filters (Monbet, 2011).

Sometimes there are seasonal effects in a series; These effects can

then be taken into account in the AR model using several methods

(Charpentier 2011; Monbet 2011).

Let us consider again our time series; An MA model is any model written in the form  where

where  ;

;  ;

;  is white noise.

is white noise.

ARMA (Autoregressive Moving Average) models were first proposed by

Box and Jenkins. This is why ARMA models are also called Box-Jenkins

models. The autoregressive and moving average models are a combination

of the AR models and the MA models.

The AR, MA, ARMA, ARIMA, SARIMA, ARMAX models are based on the

assumption of stationarity. But in reality, in financial markets

(including currency markets), we notice that the series of stock price

returns is not always stationary (Broze, 2016).

One way to challenge this hypothesis is to say that financial returns

are not stationary and therefore the residues do not follow the

movement of white noise.

Another way to look at it is to say: Even if we force the mean of the

residuals to be constant, autocovariances (and autocorrelations) are

non-zero. The individual test of nullity of autocorrelations and the

global test of nullity of autocorrelations (Statistics of Box-Pierce

(1970) and Ljung-Box (1978)) of residues show that these are

autocorrelated; This means that  : heteroscedasticity is also said to exist between the

residues. So there would be a functional link between the residues:

this is probably one of the reasons that motivated Robet Engel in 1982

to imagine the ARCH model (AutoRegressive Conditional

Heteroskedasticity). This model takes into account the

heteroscedasticity caused by volatility packages in financial markets.

The Generalized ARCH (GARCH) model is a generalized model of the

ARCH model. We also speak of Integrated GARCH (or IGARCH) when

the sum of the coefficients of the GARCH model is equal to

1.

: heteroscedasticity is also said to exist between the

residues. So there would be a functional link between the residues:

this is probably one of the reasons that motivated Robet Engel in 1982

to imagine the ARCH model (AutoRegressive Conditional

Heteroskedasticity). This model takes into account the

heteroscedasticity caused by volatility packages in financial markets.

The Generalized ARCH (GARCH) model is a generalized model of the

ARCH model. We also speak of Integrated GARCH (or IGARCH) when

the sum of the coefficients of the GARCH model is equal to

1.

Among the drawbacks of the models of the GARCH family, we can note on

the one hand that the response of the conditional variance to

innovations is linear (but in reality, innovations do not always

follow a linear process) and on the other hand that the distribution

tails produced by the GARCH model are too thick compared to the

reality observed on the markets (Fauth, 2012).

One of the solutions consists in turning to other probabilistic

models such as the regime-switching Markov models introduced by

Hamilton (1989).

In these models, it is often assumed that there are dynamic

mechanisms in the series of returns that cause the series to

"jump" from one regime to another as it moves. This means

that, on the series of yields, there are places where the series is

stationary and suddenly, a mechanism appears which causes the movement

to deviate from the general shape of its trajectory. This kind of

abrupt change of regime appears several times on the trajectory of the

yield. The origin of these sudden changes may be due to variables

exogenous to the model which have effects on the series of returns or

to stochastic mechanisms which are themselves in the series of returns

Cai (1994).

The Markov model assumes that the variable at t depends only on the

variable at t-1; This means that the Markov model assumes that there

are only first-order autocorrelations; However, in the financial

markets, we sometimes observe autocorrelations of order greater than

one. The hidden Markov model assumes that the hidden variables are not

observable, but in the economy and on the markets, we can observe and

measure the hidden or fundamental variables (Gross Domestic Product,

inflation, etc.). Gaussian, probit and/or logit models are often used

to calculate the probability that a stock price will be bullish or

bearish.

The normal distribution is characterized by: a statistically zero

mean, a median equal to the mean, a zero asymmetry coefficient (or in

English skewness) and a coefficient of flattening (or in English

kurtosis) measuring the thickness of the tails of distribution is

equal to 3 (and consequently the excess of kurtosis of a Gaussian

distribution is equal to 0). However, on the financial markets, we

notice that the series of stock prices violates these four properties

of a Gaussian distribution. This means that the average of stock

returns is not zero and that it is also different from the median.

Similarly, the stock price skewness is different from zero and the

excess kurtosis is well above zero.

Despite all these limitations, the Gaussian distribution can be

useful if we consider that the series of returns is made up of several

clusters and that the returns of each cluster follow a normal

distribution: this approach gives rise to the Gaussian mixture model

(GMM) . The Gaussian mixture model is for this purpose a weighted sum

of several Gaussians, each weighted Gaussian representing the

distribution of the returns of each cluster. The weights or weights of

the clusters represent the importance of each cluster in the overall

series of returns. The GMM and the Hidden Markov Model (HMM) are often

used together in a trading strategy to account for predictions of

future patterns of returns and regime shifts in the series of those

returns, respectively. This association gives rise to the GMM-HMM

model that we use in this article.

When no model is adequate for the dataset, a mixture model can be

used; Particularly the Gaussian mixture model as it can model any

dataset with uncertain accuracy (Vanderplas 2016; Thukral et al

2013).

Mixture models have several applications such as forecasting stock

price returns and exchange rates.

2. Research Issues and Hypotheses

Forecasting the return on an asset is not easy. Traditional time

series techniques don't always work well for predicting the

performance of an asset. One important reason is that older time

series analysis models require the data to be stationary. If it is not

stationary, we must transform the data until it becomes stationary:

this poses a problem. In practice, several phenomena are observed that

violate stationarity rules, including nonlinear processes,

seasonality, autocorrelation, and volatility clustering. This renders

most traditional models ineffective for our purposes.

2.1 Issues

Hansen (1982) already showed that the estimators of the generalized

model of moments were strongly convergent and asymptotic, under the

assumption that the observable variables are stationary and ergodic.

The GMM being a model of the family of generalized moments, we use it

in this study to predict the evolution of African currency pairs. In

other words, our objective in this article is to build a trading robot

that runs in real time around the clock from the GMM and anticipates

the evolution of returns on African currency pairs. We also integrate

the HMM model in our robot to take into account changes in Forex

regimes. The variables taken into account in our robot are on the one

hand the past returns of the African currency pairs and on the other

hand, the macroeconomic variables. The signal to buy or sell one

currency pair against another is triggered by the so-called

“mean reversion” strategy. Many financial firms are

interested in trading robots and/or empirically validating models that

they can use as a basis for developing a trading algorithm.

With the strong growth of TA and THF on the financial markets, it is

increasingly difficult for the old models developed in the literature

to anticipate trend reversals on the markets. With algorithms moving

at the speed of light in the financial markets, this way of combining

the ARMA and ARCH-family models is no longer efficient enough. Since

it is a question of our days of light, some authors then thought of

models that predict the movement of elementary particles (photons) of

it (Zhang et al, 2001). The best known of these models are the hidden

Markov models (MMC) or hidden Markov model (HMM) which are massively

used in particular in pattern recognition (imaging), in artificial

intelligence or in automatic processing of natural language

(acoustics).

2.2 GMM and return assumptions

GMM Assumptions: We assume that the GMM is flexible enough to: (1) accommodate

non-stationary processes and (2) provide a reasonable approximation of

the non-linear process generated by Forex data. We also assume in this

article that:

-

The best known mixture model is the Gaussian mixture model (GMM).

It will then be used for our study as indicated by the theme of our

study;

-

The GMM assumes that each regime (component, class, state) is

generated by a Gaussian process with parameters to be

determined;

-

The GMM uses the E-M algorithm which alternates between estimating

the parameters of the regimes (mean, variance) and the likelihood

that these parameters could reconstruct the initial data, until

there is convergence or another stopping criterion is met;

-

We will initialize the GMM with three components;

-

The trading strategy will use a total of 4 factors (or intrinsic

macroeconomic variables) to estimate the sequence of each regime and

their parameters.

Mixture models in general and GMM in particular have potential.

First, they are based on several well-established concepts. An easy

way to apply mixture models to properly anticipate asset returns is to

view asset returns as a sequence of states or regimes. Each regime is

characterized by its own descriptive statistics including average and

volatility. Said regimes must for example include low volatility and

high volatility. The assumption of the underlying model is that each

regime is generated by a Gaussian process with parameters, which we

can estimate. The GMM uses an expectation-maximization algorithm to

estimate the regime parameters and the highest probability of the

sequence of regimes.

Return Assumptions: Given the volatility of the return series in FX markets, we need a

model that does not assume that the data is stationary. Our model must

also estimate non-linear data. Gaussian mixture models seem to be

quite soft and flexible in modeling the movement of exchange rate

returns because the GMM can model any given game with uncertain

accuracy (ZeljkoIvezic 2014, Attar 2012).

In this article, we assume that:

-

Future exchange rates of one currency against another depend on

past exchange rates and Forex returns follow a non-stationary

process.

-

There is a relationship between African currencies and US interest

rates, treasury bonds, US inflation.

-

Currency pairs in Forex do not follow a random walk. Tests for the

absence of a random walk on stock prices are generally made by

Markov chains and the Wald-Wolfowitz test (1940). This hypothesis

allows us to reassure ourselves of the inefficiency of the financial

markets, in particular the Forex market. This inefficiency of the

currency market reassures us that the African currency pairs on

which we trade are anticipable, predictable and capable of

generating us good profits if we correctly predict their future

evolutions.

-

We also make the assumption that the Forex currency pair datasets

follow a normal distribution.

-

Suppose that the return of an exchange rate is a sequence of states

or regimes;

-

Each regime has its own descriptive statistics including mean and

volatility (standard deviation);

-

For a given regime, we can have for example: high volatility

(high_vol) versus low volatility (low_vol);

-

The model also assumes that at each instant t, the exchange rate

return will transit between the regimes via the probabilities; that

is, the transitions between the states of a return (bullish,

bearish, neutral) depend on the probabilities;

3. Methodological framework

In accordance with the literature, our trading robot is built from

the following data which we group into two sets: on the one hand, we

have data relating to past and present returns of African exchange

rates, and on the other hand, data providing information on

macroeconomic variables that have a significant and important effect

on exchange rates.

3.1 Data sources and samples

We call marginalized currency pair any currency pair X/Y (X and Y are

currencies) of which one of them (or both) belongs to a country (or a

region or sub-region) poor or in developing. Example: Given the

following currency pair, XAF/USD: this currency pair is considered

marginalized because the CFA Franc, therefore the ISO code is

represented by XAF, is the currency of the Central African sub-region,

which is a developing region.

Since we cannot cover all African currencies in this article[10], we propose to use the GMM to predict the future

returns of the following six currency pairs as they belong to

the African countries that have the most companies listed on African

stock exchanges[11] : South African Rand (ISO Code: ZAR), Egyptian Pound (ISO

Code: EGP), Nigerian Naira (ISO Code: NGN), Mauritian Rupee (ISO Code:

MUR), Moroccan Dirham (ISO Code: MAD) and Kenyan Shilling (ISO Code:

KES).

In this article, we will cross the above six African currencies with

the US dollar for the following reason:

The US dollar (in English, United State Dollars or USD) is the

currency with the most volume of transactions in the world. According

to the Bank for International Settlements, the daily transaction

volume on the Forex market is approximately 6.6 trillion dollars and

the daily transaction volumes for the American currency represent

nearly 2.2 trillion (BIS, 2018): this is the reason why we have chosen

to cross the six pairs of African currencies above with the American

dollar and not with another currency such as for example the euro, the

pound sterling, the yen, the yuan.

Thus, the six exchange rates whose future returns we predict in this

study are the following: USD/ZAR, USD/EGP, USD/NGN, USD/MUR, USD/MAD,

USD/KES. The notation of these six exchange rates can also be written

as follows: USDZAR, USDEGP, USDNGN, USDMUR, USDMAD, USDKES. It is this

last notation that we use when estimating and interpreting the

parameters of the GMM.

Our data on the six exchange rates above has been uploaded in real

time to the Yahoo Finance platform[12]. They therefore cover the period from January 2010 to the date of

download (i.e. 15 May 2021 at 15:30). Intuitively, it makes

perfect sense to calculate the daily returns of each exchange rate

using closing prices.

According to the Mundell-Fleming models (1963), the Dombusch model

(1976) and the Taylor rule (1993 and 1999) we retain the following 9

explanatory variables for our model:

- The Federal Funds Target Rate (DFEDTAR) interest rate target;

- The maximum interest rate target of the FED (or in English, Federal

Funds Target Range - Upper Limit, DFEDTARU);

- The Federal Funds Target Range - Lower Limit, DFEDTARL;

- The effective interest rate of the USA (or in English, Effective

Federal Funds Rate, EFFR);

- The difference between the borrowing interest rate and the lending

interest rate;

- The interest rate spread (difference between the effective US

interest rate and the interest rate desired by the FED) (or in

English, TED Spread, TEDRATE);

- The difference between 10-Year Treasury Constant Maturity Minus

2-Year Treasury Constant Maturity, T10Y2Y and 10-Year Treasury

Constant Maturity Minus 2-Year Treasury Bonds;

- The difference between 10-Year Treasury Constant Maturity Minus

3-Month Treasury Constant Maturity US Treasury Bonds and 3-Month

Constant Maturity US Treasury Bonds (T10Y3M);

- The expected US inflation rate over 5 years (or in English: 5-Year,

5-Year Forward Inflation Expectation Rate; T5YIFR);

We have chosen US treasury bills and US interest rates as explanatory

variables in the GMM model of our daytrading strategy because: on the

one hand, African central banks and the public treasuries of African

countries publish quarterly data (or monthly) on treasury bills and on

interest rates and on the other hand, our strategy requires daily

data.

Our data on the nine financial variables above has been uploaded in

real time from the US Federal Reserve (FED) website[13]. They therefore cover the period from January 2010 to the date of

download (i.e. May 15, 2021 at 3:30 pm).

3.2 Model estimation

Let be a series of exchange rates;

We define exchange rate returns at a point in time  given, as follows:

given, as follows:

And let us note  avec

avec  ;

;

The latent model is written:

,

,  (3.2)

(3.2)

Thresholds :

si  alors

alors  ; In this case, the return is said to be bullish

; In this case, the return is said to be bullish

si  alors

alors  ; In this case, the return is said to be neutral (almost rare

case on foreign exchange markets)

; In this case, the return is said to be neutral (almost rare

case on foreign exchange markets)

si  then

then  ; In this case, the return is said to be bearish

; In this case, the return is said to be bearish

where  is the latent variable and represents the propensity of a

return to transit from a bearish state to a bullish state or vice

versa (assuming that we disregard the case where). This depends a priori linearly on individual characteristics X and

unobservable factors

is the latent variable and represents the propensity of a

return to transit from a bearish state to a bullish state or vice

versa (assuming that we disregard the case where). This depends a priori linearly on individual characteristics X and

unobservable factors . The

. The  represent the economic factors that affect exchange rates

(expected inflation rate, interest rate, GDP,...).

represent the economic factors that affect exchange rates

(expected inflation rate, interest rate, GDP,...).  ;

;  ;

;  represents the mathematical expectation operator.

represents the mathematical expectation operator.

Having defined the different thresholds, we can write the latent

model in a reduced form as follows:

Let be the following diagram, inspired by Renals et al (2013):

This diagram is a simplified representation of a hidden Markov

model (HMM) where  represent the hidden variables that generate the current states

of the series

represent the hidden variables that generate the current states

of the series . In our study, represent the macroeconomic variables selected in subsection

3.1 and the series represents the exchange rate return series. The

. In our study, represent the macroeconomic variables selected in subsection

3.1 and the series represents the exchange rate return series. The  represent the probabilities that a state will remain unchanged. The

represent the probabilities that a state will remain unchanged. The  et les

et les represent the probabilities of transition from one state to

another (the two states are different).

represent the probabilities of transition from one state to

another (the two states are different).

The return  can follow one of the following distributions:

can follow one of the following distributions:

-

Multivariate Gaussian model without cluster with mean

and covariance matrix

and covariance matrix  :

:

(The latent model and thresholds are those of equation 3.2)

et

et  (3.3)

(3.3)

With  : we can say that

: we can say that  follows a reduced centered normal distribution;

follows a reduced centered normal distribution;  represent the probabilities of transitions between factor

vectors

represent the probabilities of transitions between factor

vectors  ;

;  is the probability density function of returns

is the probability density function of returns  ; also measures the likelihood that the return will be bullish ;

; also measures the likelihood that the return will be bullish ;  : returns are said to follow a normal distribution with mean and covariance matrix ;

: returns are said to follow a normal distribution with mean and covariance matrix ;

-

Gaussian mixture model with M components, mean

and covariance matrix

and covariance matrix  :

:

In this case, we have two latent models: on the one hand, we note a

model that takes into account the components  and on the other hand, we have a model that takes into account the

subset of returns belonging to a component.

and on the other hand, we have a model that takes into account the

subset of returns belonging to a component.

On the one hand, we note:

,

,  (3.4)

(3.4)

where  are reals; The

are reals; The  always represent macroeconomic variables and

always represent macroeconomic variables and  is a Gaussian white noise;

is a Gaussian white noise;

The thresholds can be defined as follows:

If  then

then  ;

;

If  then

then  ;

;

…. ….

….

If  then

then  ;

;

If  then

then  ;

;

For a dataset with M clusters or components, the threshold numbers

are M-1.  is the latent variable and represents the transition propensity

from one cluster to another. This depends a priori in a linear manner

on the characteristics x of each return and on non-observable factors . The represent the macroeconomic factors that affect exchange rates

(expected inflation rate, interest rate, GDP,...).

is the latent variable and represents the transition propensity

from one cluster to another. This depends a priori in a linear manner

on the characteristics x of each return and on non-observable factors . The represent the macroeconomic factors that affect exchange rates

(expected inflation rate, interest rate, GDP,...).  ;

;  ; represents the mathematical expectation operator.

; represents the mathematical expectation operator.

The general reduced form of the latent model (3.4) is written:

The above inequalities describing thresholds can be generalized as

follows:

If  then

then  with

with  ;

;  and

and  ;

;

With  ; The

; The  can be numeric values, strings, alphanumeric data, ordered or

not. They are only there to represent the different clusters.

can be numeric values, strings, alphanumeric data, ordered or

not. They are only there to represent the different clusters.

This system clearly shows that the expressions  and

and  differ only with thresholds

differ only with thresholds  and

and  ;

;

And on the other hand, we have:

(3.5)

(3.5)

Where  and

and  is a Gaussian white noise; The latent model is said to be an

ARMA process (p, q). The thresholds are defined as follows (these

thresholds are those presented in equation 3.2 associated this time

with an ARMA model (p, q) and not a multidimensional linear model):

is a Gaussian white noise; The latent model is said to be an

ARMA process (p, q). The thresholds are defined as follows (these

thresholds are those presented in equation 3.2 associated this time

with an ARMA model (p, q) and not a multidimensional linear model):

If then ; In this case, the return is said to be bullish

If then ; In this case, the return is said to be neutral (almost rare

case on foreign exchange markets)

If then ; In this case, the return is said to be bearish

where  is the latent variable and represents the propensity of a

return to transit from a bearish state to a bullish state or vice

versa (assuming that we disregard the case where). And the reduced form of this latent model can be written as

follows:

is the latent variable and represents the propensity of a

return to transit from a bearish state to a bullish state or vice

versa (assuming that we disregard the case where). And the reduced form of this latent model can be written as

follows:

Let say  and

and  ;

and

;

and  et

et  ;

;

is the centered-reduced variable of the values x

belonging to the cluster m;

is the centered-reduced variable of the values x

belonging to the cluster m;

is the centered-reduced variable of the returns r belonging to

the cluster m.

is the centered-reduced variable of the returns r belonging to

the cluster m.

Given these two latent models, we can write the M-component mixture

model as follows:

(3.6)

(3.6)

3.3 Calculation of GMM parameters

We will see later that  is a function of ;

is a function of ;  : the returns belonging to each cluster are said to follow a

normal distribution with mean and covariance matrix

: the returns belonging to each cluster are said to follow a

normal distribution with mean and covariance matrix  ; The represent the probabilities or weights of the components

; The represent the probabilities or weights of the components  ;

;  represents the probability that a return will be bullish when know the vector of macroeconomic variables

represents the probability that a return will be bullish when know the vector of macroeconomic variables  ;

;

The solution of the system of equations (3.6) involves three

concepts: conditional probabilities  that represent the probability that a return belongs to a class (with

that represent the probability that a return belongs to a class (with  ) , the Markov model for determining transition

probabilities between the (this model is also used to determine transition probabilities

) , the Markov model for determining transition

probabilities between the (this model is also used to determine transition probabilities  between returns

between returns  ;

;  ) and the hidden Markov model (HMM) to determine transition

probabilities

) and the hidden Markov model (HMM) to determine transition

probabilities  between and . But these notions cannot be used independently of each other.

between and . But these notions cannot be used independently of each other.

The simultaneous consideration of these three notions when solving

the system (3.6) can be done using the following techniques or methods

(Renals et al, 2013): recursive methods forward, backward, the Viterbi

algorithm, the Expectation-Maximization (E-M) algorithm.

By applying the E-M algorithm to the system of equation (3.6), we

obtain the following proportions as in the work of Renals et al

(2013):

-

Probability that a vector of macroeconomic variables belongs to a cluster

;

;  (3.7)

(3.7)

with  the probability density of the centered-reduced normal

distribution modeling the series of macroeconomic variables of a cluster ; and and ;

the probability density of the centered-reduced normal

distribution modeling the series of macroeconomic variables of a cluster ; and and ;

-

Probability that a return belongs to a cluster : It is also the probability that a return will be bullish or

bearish or neutral.

(3.8)

(3.8)

With and  is the probability density of a centered-reduced normal distribution

modeling this time the series of returns of a cluster and macroeconomic variables that are in the latent model

is the probability density of a centered-reduced normal distribution

modeling this time the series of returns of a cluster and macroeconomic variables that are in the latent model ,

,  .

.

-

The means of the different clusters:

(3.9)

(3.9)

- The elements of the

variance-covariance matrix:

(3.10)

(3.10)

With  et

et  ; is always presented in the same way as in the case of equation

(3.8).

; is always presented in the same way as in the case of equation

(3.8).

-

The coefficients of the mixture are re-estimated in a similar way

to transition probabilities:

(3.11)

(3.11)

By replacing equations (3.8), (3.9), (3.10) and (3.11) with their

values in the system (3.6), we find the final probabilities . In practice, we often initialize

. In practice, we often initialize  with

with  in step zero of the E-M algorithm (ZeljkoIvezic et al,

2014).

in step zero of the E-M algorithm (ZeljkoIvezic et al,

2014).

Given a series of returns and a series of macroeconomic variable vectors  , the future probability of an expected return can be estimated

at any time. To archive this objective, it is necessary to determine a

threshold making it possible to discriminate the returns according to

their state (bullish or bearish). The threshold can be determined with

the ROC curve by making a trade-off between sensitivity and minus

specificity.

, the future probability of an expected return can be estimated

at any time. To archive this objective, it is necessary to determine a

threshold making it possible to discriminate the returns according to

their state (bullish or bearish). The threshold can be determined with

the ROC curve by making a trade-off between sensitivity and minus

specificity.

3.4. Deployment of the robot in production on the production

market

We chose to backtest our data with anaconda, jupiter lab, and the

programming language python. The code of the robot we deployed in

production is written in python. There is nothing better to understand

the foreign exchange markets than to have the "Full skin inside

the Game"[14] and to go out in "Black Boxes" and theories (Taleb,

2018). The previous sentence motivated us to open a real account with

an exchange operating on the foreign exchange market and to deposit a

very small capital of ten thousand euros, or a capital of around six

million five hundred CFA francs. To connect our robot to this

exchange, we deposited our robot on a red hat 8.6 linux operating

system embedded in an ec2 t2.micro server provided by the Amazon Web

Services cloud provider.

It cannot be said enough in the financial markets: "always

protect your capital against the drawdown or against a six sigma or

against a sudden sharp rise in prices [15] or against a sudden sharp drop in prices". This sentence

motivated us to implement trailing stop loss to protect our earnings

as well as our capital. The calculation of the probability that our

robot wins or not on a day is done by taking the PNL history of our

robot and passing this history as input in a machine learning

algorithm developed by Chan et al (2021).

4. Results of estimates

Each of the six exchange rates we selected in subsection 3.1 is

explained both by its own past values and by the nine

financial variables presented in subsection 3.1.

The GMM can take into account the non-linearity or the presence of

clusters on the six currency pairs. The determination of the optimal

number of components of the six exchange rates will be done directly

during the estimation of the GMM parameters.

4.1. Estimation of the different GMM parameters

The GMM has the particularity that it first classifies the data into

clusters and then calculates the weights (probabilities ) of each cluster based on the financial variables that explain the

returns belonging to that cluster. Then the GMM calculates the

probability of achieving a return from the variables of each cluster

(past returns for the ARMA part and economic variables for the latent

model of cluster weights ) and the normal distribution parameters of that cluster.

) of each cluster based on the financial variables that explain the

returns belonging to that cluster. Then the GMM calculates the

probability of achieving a return from the variables of each cluster

(past returns for the ARMA part and economic variables for the latent

model of cluster weights ) and the normal distribution parameters of that cluster.

In Table 1 below, we have used the returns of the 6 African currency

pairs and applied the GMM to these pairs assuming that there are three

representative components: Low Volatility, Neutral Volatility and

Volatility strong. The choice of this number was made on the basis of

the optimal number of components retained by the AIC and the BIC

(remember that this number is equal to three).

Table 1: Estimation of the parameters of the different components of the

GMM

|

|

USDZAR_lret

|

USDNGN_lret

|

USDEGP_lret

|

USDMAD_lret

|

USDMUR_lret

|

USDKES_lret

|

|

0th hidden state

|

Mean

|

2,2759.10-04

|

6,1194.10-05

|

0,0058.10-00

|

7,3433.10-04

|

-1,4272.10-04

|

1,4596.10-04

|

|

variance

|

1,1590.10-04

|

1,4266.10-05.

|

0,0027.10-00

|

2,6375.10-04

|

3,9138.10-05

|

1,3882.10-05

|

|

1st hidden

state

|

Mean

|

1,3140.10-04

|

7,6048.10-05

|

-3,6772.10-05

|

2,2056.10-04

|

2,2564.10-04

|

2,7480.10-05

|

|

variance

|

5,6064.10-05

|

5,2360.10-05

|

4,1210.10-06

|

0,0002.10-00

|

9,4292.10-05

|

5,6250.10-05

|

|

2nd hidden state

|

Mean

|

0,0010.10-00

|

0,0027.10-00

|

5,0942.10-04

|

0.0004.10-00

|

5,2738.10-04

|

0,7282.10-00

|

|

variance

|

0,0001.10-00

|

0,0011.10-00

|

5,9591.10-05

|

0.0001.10-00

|

1,4202.10-04

|

7.6688.10-00

|

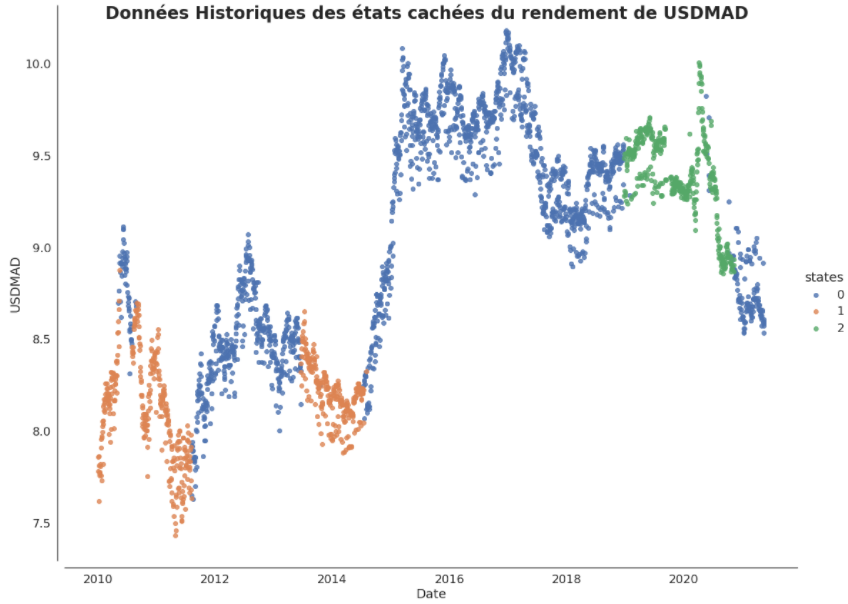

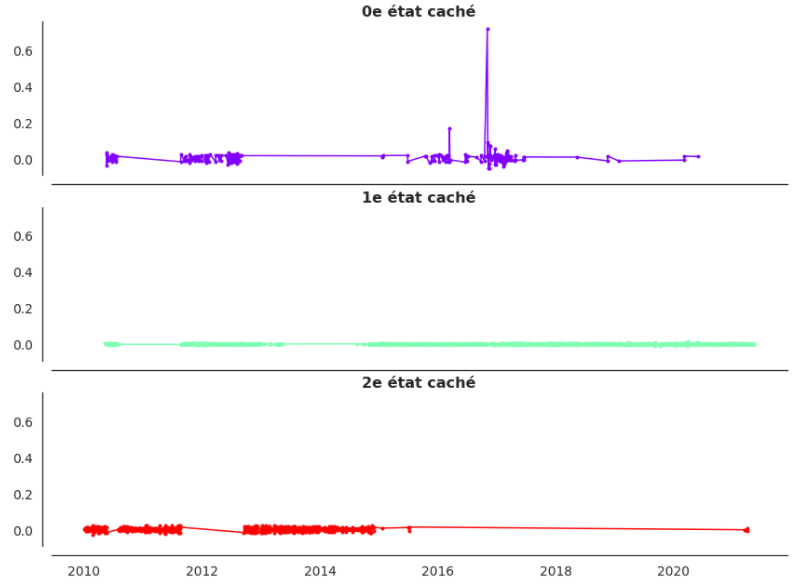

Chart 1: Hidden states of USDMAD pair returns

For the hidden states of the returns of the other 5 currency pairs,

reference can be made to Chart 2 in the appendix.

The following comparison is made between the hidden states of the

USDMAD pair: The zero state or “zero regime” with the highest average

and the highest variance: it then represents our high volatility

regime. Regime 1 is like our neutral volatility regime because its

variance ranks second. And regime 2 is like our low volatility regime

because its mean is ranked second and its variance is ranked last

among the USDMAD hidden state variances. Thus, we can say that the GMM

adapts better to non-stationarity on the USD/MAD pair. The GMM

classifies returns into low, neutral and high volatility, giving for

each group or regime its mean and its variance.

We can then generalize by saying that the GMM takes into account the

non-stationarity of the 6 currency pairs.

4.2. Prediction of the evolution of yields

A return lying above the upper limit of the confidence interval of

the Johnson Su distribution (1949) or the Gaussian distribution is

called outlier too_high and will be called outlier too_low when it is

below the lower limit the confidence interval of this distribution. A

too_high outlier can be either negative or positive; A too_low outlier

can also be either negative or positive. By exploiting the fact that

the returns are generally close to zero, one can simply compare the

sums in absolute value of the positive outliers and the negative

outliers. If the ratio between the sum in absolute value of the

positive outliers and the sum in absolute value of the negative

outliers is greater than 1, this means that the returns are globally

bullish, otherwise, they are globally bearish. The ratios in absolute

value between the sum of the positive outliers and the sum of the

negative outliers of the returns of the six currency pairs in the

table above are greater than 1 and therefore show for this purpose

that the returns of these currency pairs are in general bullish (see

appendix, Table 2 for more details).

The calculation of the percentage of errors of the “correctly

predicted” returns with the validation data can be paraphrased

as follows: To evaluate our results globally, we have:

- Evaluate the forecast error of each currency pair for forecasts

over 1 or 5 periods (days) ahead. In other words, we have evaluated

the error of the forecasts of each currency pair at D+1 or D+5 in the

future.

- Globally evaluate the forecast error of all the 6 currency pairs

selected for the forecasts 1 or 5 periods ahead. In other words, we

have globally evaluated the forecast error of all 6 currency pairs at

Day+1 or Day+5 in the future.

Table 3: GMM with 4 factors or explanatory variables

|

|

Model: GMM | Variable explained: exchange rate returns |

Factors: TEDRATE, T10Y2Y, T10Y3M, T5YIFR | Data sources: Yahoo Finance and FRED | Number of

components: 2 | Step: 1 or 5 | Lookback: 1 | Significance

threshold: 1% | Cutoff: 2019 | start_date :01/01/2010 |

end_date: 15/05/2021;

|

|

Currency pairs

|

USDZAR_lret

|

USDNGN_lret

|

USDEGP_lret

|

USDMAD_lret

|

USDMUR_lret

|

USDKES_lret

|

|

Degree of accuracy of the GMM

|

73,887%

|

66,766%

|

32,344%

|

61,721%

|

51,929%

|

51,632%

|

|

Sum of errors

|

88

|

112

|

228

|

129

|

162

|

163

|

Table 3 above presents the percentages of precision of the forecasts

of the evolutions made on the six exchange rates studied in this

article. These changes are explained on the one hand by past exchange

rates (previous) and on the other hand by the following 4 explanatory

variables: TEDRATE, T10Y2Y, T10Y3M, T5YIFR.

A sample of USDNGN currency pair returns from 01/01/2010 to

05/15/2021, shows that the GMM estimates USDNGN currency pair returns

with an accuracy of 72.700% (To obtain this result, we used the 7

financial variables: DFEDTARU, DFEDTARL, EFFR, TEDRATE, T10Y2Y,

T10Y3M, T5YIFR).

It can also be seen in Table 3 above that the GMM-HMM predicts the

movement of the USDZAR pair with a high level of accuracy of 73.887%.

This clearly shows that exchange rate returns are predictable and they

do not follow a random walk.

We can then generalize by saying that returns on exchange rates do

not follow a random walk (we also say that the Forex market is

inefficient) if we predict them with models such as the GMM or GMM-

HMM.

From the last paragraph of subsection 4.1 and from the paragraph

above, we can state on the one hand that the assumptions made in

subsection 2.1 (concerning GMM and yields) are validated and on the

other hand, that we predict very well the future evolutions of

exchange rate returns. And therefore, this explains the fact that our

robot built from the GMM-HMM model generates overall positive daily

profits.

See Chart 3 in the appendix for charts of return forecasts made on

the other 5 currency pairs.

4.3 Measures of Investment Risk: Sharpe Ratio and Other

Indicators

Table 4: Some Risk Measures on Currency Pair Prediction

|

Mesures

|

USDZAR_lret

|

USDNGN_lret

|

USDEGP_lret

|

USDMAD_lret

|

USDMUR_lret

|

USDKES_lret

|

|

Sharpe ratio

|

1.531

|

1.561

|

1.501

|

1.545

|

1.503

|

1.520

|

|

Market Beta

|

0.007

|

0.004

|

0.001

|

0.001

|

-0.002

|

0.014

|

|

Value at risk or VaR (0.05)

|

0.057

|

0.052

|

0.0502

|

0.054

|

0.051

|

0.044

|

|

Covariance VaR (0.05)

|

0.027

|

0.025

|

0.023

|

0.026

|

0.024

|

0.0213

|

Table 4 above shows that all the 6 currency pairs studied in this

work have a Sharpe ratio greater than 1 and therefore their different

expected returns would be greater than the risks incurred on these

currency pairs for an investor. Although there is great volatility in

these 6 currency pairs, this ratio shows us that the expected return

on an investment in these pairs is positive. The market betas are very

low and show that the returns on these currency pairs are weakly

dependent on the Forex market (due to the correlation between the

currency pairs or the multicollinearity between the currency pairs).

This also means that the volatility on these currency pairs also

depends on other variables such as macroeconomic indicators of

monetary and fiscal policies.

The value at risk coefficients and the value at risk variance

covariance matrix are very low (around 5%) and clearly show that the

minimal risk that an investor is prepared to take when investing in

these pairs currency is acceptable. (See appendix, Table 5 for other

statistical risk measurement indicators).

Conclusion

This article was about building a Daytrading strategy by applying a

Gaussian mixture model to the following six marginalized currency

pairs: USDZAR, USDNGN, USDEGP, USDMAD, USDMUR and USDKES. After

reviewing the financial literature, we believe that this is the first

time in the financial literature that a robot built from the GMM-HMM

and trading on African currency pairs (and running in real time 24/7

24 in the Forex market) was developed (coded) and published by

researchers. The Gaussian Mixture Model (GMM) we use here is a

Gaussian Hidden Variables Mixture Model (much like a model combining

the Gaussian Mixture Model and the Hidden Markov Model or GMM-HMM)

because we estimated the returns exchange rates assuming that these

can be explained on the one hand by their past returns and on the

other hand by macroeconomic variables. We found that the GMM-HMM

estimates returns for the USDZAR currency pair with 73.887% accuracy

and the USDNGN currency pair with 72.700% accuracy.

The generally positive performance of the trading algorithm (robot)

that we developed during this article convinced us to open our trading

robot to natural and legal persons.

Based on the results of our estimates and the validation of our

assumptions by these results, we can confidently recommend the

attraction of foreign capital by African states and the African

private sector. For this, on the one hand, African states must

supervise, facilitate and make more flexible the procedures for

creating asset management and algorithmic trading companies, and, on

the other hand, the African private sector must make the effort to

trust these asset management (and algorithmic trading) companies to

manage a part of their financial assets (even if it is only a very

small fraction).

References

Adam Smith (1759); Theory of Moral Sentiments

Adam Smith (1776); Researches on the nature and causes of the wealth

of nations

Akerlof, George A. “The Market for ‘Lemons’:

Quality Uncertainty and the Market Mechanism.” The Quarterly

Journal of Economics, vol. 84, no. 3, 1970, p. 488–500. JSTOR,

https://doi.org/10.2307/1879431. In American slang, a lemon is a car

that is found to be defective after it has been bought.

Ali El Attar. Robust estimation of mixing models on distributed data.

Learning [cs.LG]. University of Nantes, 2012. French.

<tel-00746118>

Arthur Charpentier: Time series forecasting models; UQAM, ACT6420,

Winter 2011; May 15, 2012; charpentier.arthur@uqam.ca, url:

http://freakonometrics.blog.free

Bank of International Settlement, (2004), BIS Quarterly Review

– International banking and financial market

developments.

Bank of International Settlement, (2019), Triennial Central Bank

Survey-Foreign exchange and derivatives market activity in 2019.

Baum, L.E.; Petrie, T. (1966). "Statistical Inference for

Probabilistic Functions of Finite State Markov Chains"

BIS Papers No 90; Foreign exchange liquidity in the Americas;

https://www.bis.org/publ/bppdf/bispap90.pdf; March 2017

Carl Edward Rasmussen: The Infinite Gaussian Mixture Model;

Department of Mathematical Modeling; Technical University of Denmark;

Building 321, DK-2800 Kongens Lyngby, Denmark carl@imm.dtu.dk; MIT

Press (2000);

https://groups.seas.harvard.edu/courses/cs281/papers/rasmussen-1999a.pdf

Chan Ernest and Belov Sergei and Ciobanu Radu, Conditional Parameter

Optimization: Adapting a Strategy to Different Market Regimes (April

14, 2021). Available at SSRN: https://ssrn.com/abstract=3880643;

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3880643;

https://www.predictnow.ai/blog/conditional-parameter-optimization-adapting-parameters-to-changing-market-regimes/

David Guerreiro: FOREIGN EXCHANGE MARKET BASICS: Financial

Techniques; Year 2015-2016 Paris 8 University;

david.guerreiro@univ-paris8.fr

Davis, Mark, and Alison Etheridge. “Mathematics and

Finance.” Louis Bachelier's Theory of Speculation: The

Origins of Modern Finance, Princeton University Press, 2006, pp.

1–14. JSTOR, http://www.jstor.org/stable/j.ctt7scn4.5.

Demsetz, H. (1968). The costs of transacting. Quarterly Journal of

Economics, Vol.82, 33-53.

Douglas A. Reynolds et al: Speaker Verification Using Adapted

Gaussian Mixture Models; M.I.T. Lincoln Laboratory, 244 Wood St.,

Lexington, Mass. 02420; Digital Signal Processing 10, 19–41

(2000)

Eriksson, S. and Roding, C., (2007), Algorithmic Trading Uncovered -

Impacts on an Electronic Exchange of Increasing Automation in Futures

Trading, Royal Institute of Technology, Stockholm.

Eugène Fama: "Efficient Capital Market: a Review of

Theorical and empirical Works", 1970

German, M.B. (1976). Market microstructure. Journal of Financial

Economics, 3, pp 257-275

Hamilton, James D. “A New Approach to the Economic Analysis of

Nonstationary Time Series and the Business Cycle.” Econometrica,

vol. 57, no. 2, 1989, p. 357–84.

Hendershott, T., (2003), Electronic Trading in Financial Markets,

IEEE Computer Science.

Jake Vanderplas: "Python Data Science Handbook "ESSENTIAL

TOOLS FOR WORKING WITH DATA [2016]; [p. 476 to 488]

John B. Taylor (January 1999) “A Historical Analysis of

Monetary Policy Rules”; p. 319 – 348; URL:

https://www.nber.org/system/files/chapters/c7419/c7419.pdf

John B. Taylor, Discretion versus policy rules in practice (1993),

Stanford University, y, Stanford, CA 94905

Johnson, N.L. (1949). "Bivariate Distributions Based on Simple

Translation Systems".

Johnson, N.L. (1949). "Systems of Frequency Curves Generated by

Methods of Translation";

https://www.jstor.org/stable/pdf/2332539.pdf

Jun Cai: A Markov Model of Switching-Regime ARCH; Journal of Business

& Economic Statistics, Vol. 12, No. 3. (Jul., 1994), p.

309-316

Lars Peter Hansen: "Large sample properties of generalized

method of moments estimators". Vol.50, No. 4 (July 1982) p.

1029-1054

Laurence Broze: Econometrics of finance and nonlinear time series;

University of Lille 3;

https://moodle.univ-lille3.fr/pluginfile.php/381970/mod_resource/content/1/Poly1_2016.pdf;

2016-2017

Laurence Broze: Scoring methods and risk management; University of

Lille 3;

https://moodle.univ-lille3.fr/pluginfile.php/392292/mod_resource/content/1/Credit2016.pdf;

2016-2017

Lexis Fauth: High Frequency Trading Modeling and Statistical

Arbitrage; University of Lille I; Master 2 Mathematics and Finance

Mathematics of Risk 2012/2013

Lofgren, Karl-Gustaf, et al. “Markets with Asymmetric

Information: The Contributions of George Akerlof, Michael Spence and

Joseph Stiglitz.” The Scandinavian Journal of Economics, vol.

104, no. 2, 2002, p. 195–211. JSTOR,

http://www.jstor.org/stable/3441066.

Lovjit Thukral, Hélyette German et al: "A daily Trading

strategy in the ETN space", summer 2013, journal of

trading.

Markov, A. A. 1913. An example of statistical investigation of the

text Eugene Onegin concerning the connection of samples in chains. (In